The holiday season definitely tops the list of my favorite times of year, second maybe only to summer. But whether you’re sitting on a beach counting money or keeping the heat off to save pennies, there are some key financial steps for content creators to consider before the end of the year comes.

Potential Financial Steps for Content Creators This Month

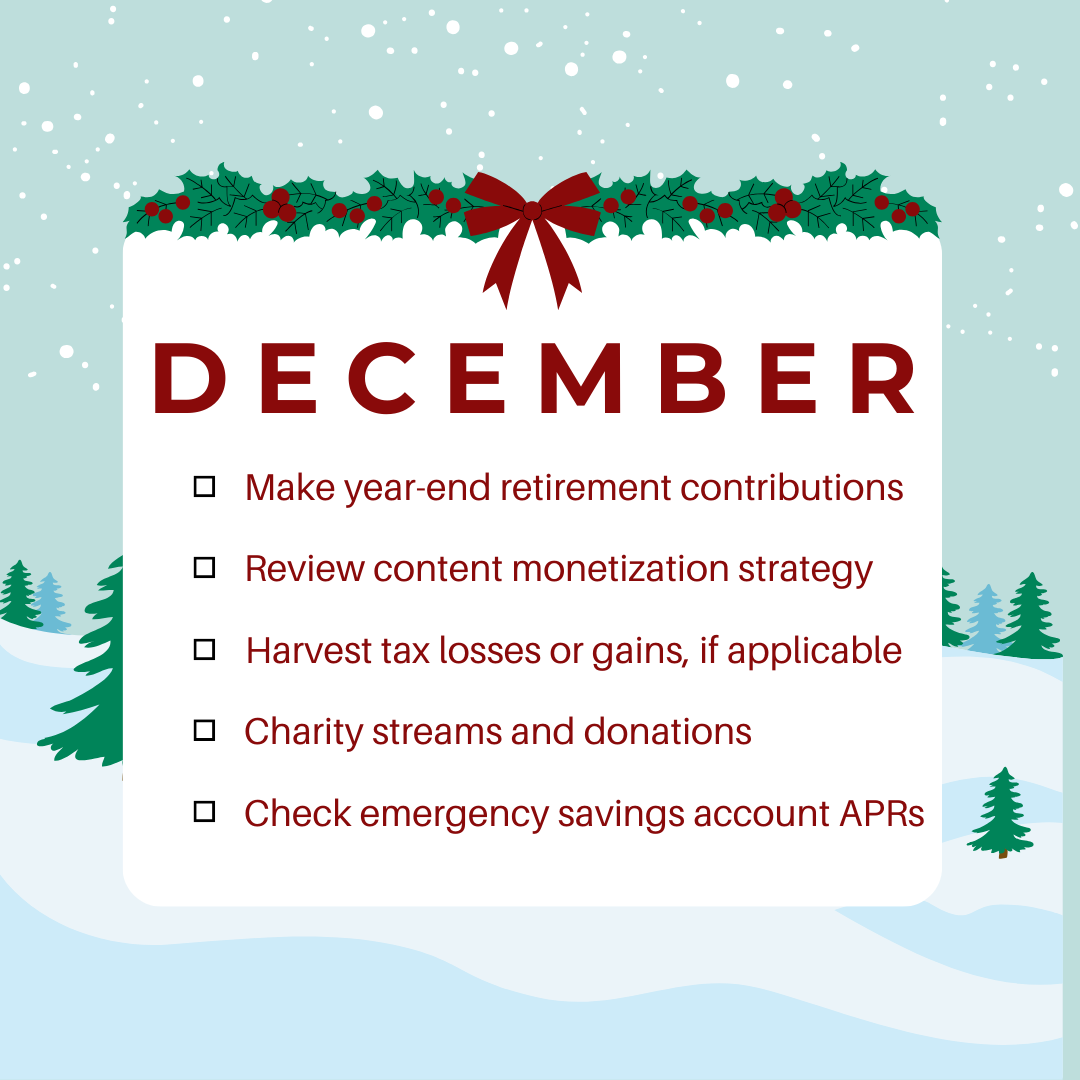

Financial steps content creators might take in December include:

- Update year-end retirement contributions

- Review content monetization strategy

- Harvest tax losses or gains, if applicable

- Charity Streams and Donations

- Review Your Emergency Fund APRs

1. Optimize Retirement Contributions

Business Retirement Plans - 401(k), SEP-IRA

As business owners, content creators have a huge opportunity in this area.

Think of how a normal employer usually offers its employees a 401(k) – well, in your case, you own the business, so you have the same option!

So, with year-end approaching, if your goal is to max out these accounts make sure you’re on track.

If you don’t have one setup yet, there’s still time. You either have until 12/31 or until your tax deadline, depending on the type of retirement account you set up.

What’s the benefit? Quick example:

If your marginal tax rate is 24%, every dollar you contribute to a tax-deferred retirement plan (like a SEP-IRA or 401(k)) would reduce the taxes you owe by 24 cents. So, a $10,000 contribution could lower your tax bill by $2,400!

Individual Retirement Account (IRA)

Just like the name says, these are accounts for individuals – separate from your business retirement plan. And, yes, you can have both!

There are two types:

- Traditional: Pre-tax, like a 401(k)

- Roth: After-tax

The tax benefits of a Traditional IRA work just like a 401(k) or SEP-IRA in the example above.

The tax benefits of a Roth IRA are the opposite. Using our example above, a contribution to a Roth IRA would increase your tax bill by 24 cents for every dollar.

Why would you want to pay more taxes? In this case, if you’re in a lower tax bracket now than you expect to be in the future, it may be beneficial to pay now and have the earnings grow tax-free.

The deadline to contribute to IRAs is usually tax day, but it may make sense to do it now! Remember, it also takes time to setup the account and doing it now can help avoid a time crunch later.

2. Review content monetization strategy

How did your business do this year? Did you make more or less than you expected?

December is a perfect time to zoom out and reflect, particularly around your content and how you’re monetizing it.

Some questions I find helpful are:

- What is your main source of income (like AdSense, Twitch Subs, etc.)?

- Are you doing everything you can to maximize this source?

- If so, are there new areas you can explore adding for next year? See what viewers are asking for in comments, Discord, etc.

- If not, what changes can you make to your content creation strategy for next year?

Running a business is a game of adaptation. If you’re not constantly innovating, you’re falling behind. Content creation is at the forefront of this.

The end of the year is a perfect time to look back at your analytics and qualitative data to adapt and get ready to tackle the upcoming year.

3. Harvest tax losses or gains, if applicable

Tax loss harvesting is a bit counterintuitive – I mean nobody likes to lose money on investments, right?

But, this tax tip can be a way to pull a win out of some losers. How can you use it?

Since the IRS only taxes you on your net investment profits for the calendar year (i.e. investment profits minus losses), any stocks you sell at a loss during the year can offset those you sold at a gain.

So, if you sold investment(s) and are facing a big capital gain, it may be beneficial to sell any losers and offset the taxes you’ll owe.

This is especially important if your capital gains tax rate will be higher than your ordinary income tax rate.

Vice-versa, if this is a low-income year for you, Tax Gain Harvesting by selling an investment at a gain can increase your taxable income.

The deadline to do this is 12/31, which makes December an ideal time to look back at your investments!

4. Charity Streams and Donations

Only Ebenezer Scrooge would strategize around charity, right??

Not quite!

You may have heard that charitable donations are tax-deductible. Not so fast – there are restrictions around deducting donations (e.g. you have to itemize deductions on your return).

If you’re donating enough to do that, you really want to take the time first to strategize the best way to go about it.

For example, it may be more beneficial to donate a large amount in one year instead of small donations spread out over multiple years.

You’ll also want to be sure that the organization you’re giving to is a not for profit 501(c)(3).

Charity Streams

Keep in mind that if you do a charity stream, those proceeds are not tax-deductible to you the streamer.

The only way this would be deductible is if you physically collected donations from viewers yourself (therefore increasing your personal taxable income) and donating to the charity yourself. We do not recommend doing this.

If you want to do a charity stream, we recommend using a service like Tiltify that helps you facilitate donations directly to the charitable organization! Glance through their best practices for a charity stream before you do yours.

In the end, no matter how big or small your donation, this is a wonderful time of year to support our fellow humans who need it. 1Up has supported charities like Operation HOPE that help teach financial literacy, if you’re looking for a great cause!

5. Optimize Your Emergency Fund

An emergency fund is a must-have financial safety net for every creator.

As a self-employed person your business revenue is your lifeblood and, if things slow down and you’re not prepared, it can literally affect how you live.

So while you’re tending to other areas, don’t overlook the simple things like your emergency fund.

Check the annual percentage rates (APRs) of your savings accounts – and if you don’t have a high yield savings account, GET ONE.

As of the end of 2023, if your emergency fund is non-existent or not earning somewhere around 4-5% APR, consider making adjustments.

Reflect on Financial Goals

As the year concludes, now is the perfect time to reflect on your overall financial goals too.

Most importantly, celebrate the wins you’ve had (no matter how big or small) and the milestones you’ve achieved.

We also want you to DREAM BIG. Money itself is not the end, but a tool to get there. That’s why in our goals-based approach, we help clients dream up and plan for the big, hairy, audacious thing you want.

In wrapping up 2023, these financial steps help content creators ensure you’re not just working hard but turning your efforts into a solid financial foundation.

What's Missing?

Is anything miss from this list? If so, please let me know!

If you’re interested in a review of your specific situation…